When I heard that Lehman and AIG were going under (or being nationalized in the case of AIG) I knew that the era of Milton Friedman was at an end. Unregulated markets designed to maximize short-term profit above all else always collapse under their own weight. As a friend at one of the last remaining investment banks so eloquently put it, "It's the government's own damn fault anyway for not expecting the free market to be greedy - I mean, that's the point, right?"

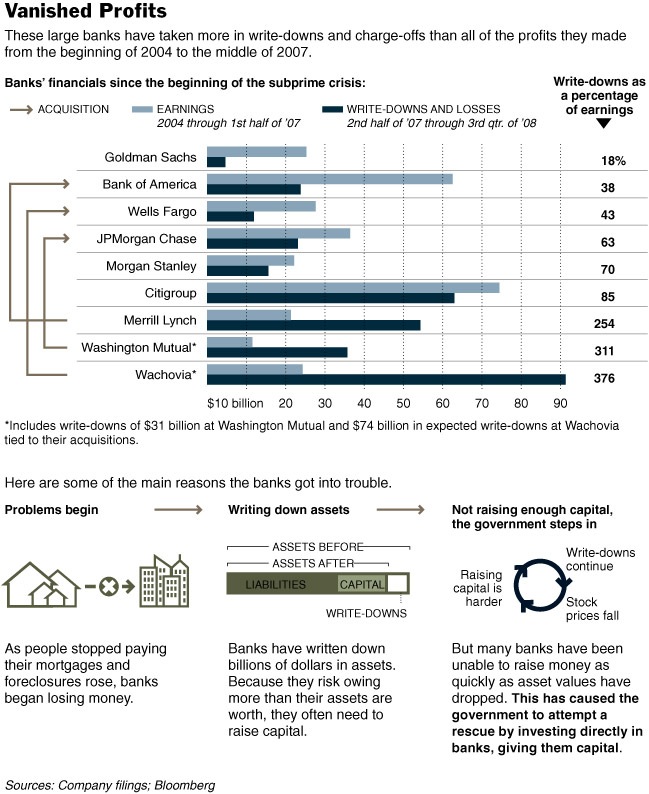

But unchecked greed will get even the greedy into trouble. As this graph shows, it wasn't in the interest of these bankers to effectively lose as much money as they've gained since 2004.

(We should all be outraged that a few CEOs and managers have been rewarded to the tune of millions of dollars for losing as much money as they made. Bailout using tax payer dollars while not going after these ill-gotten gains is effectively a subsidy from the poor to the rich. But I digress.)

After the demise of the current system, we're back where we were circa 1960, i.e. Keynesian economics. John Maynard Keynes was a well-regarded economist who developed much of what we now know as the discipline of economics, including the entire discipline of macroeconomics. Keynesian economics argues that the state can play a role - sometimes a major role - in building up the private sector and in stimulating economic growth.

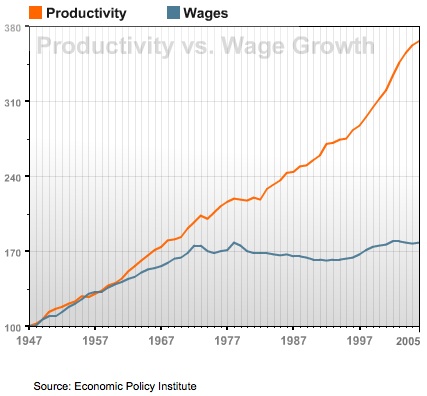

After the depression, World War II and the Bretton Woods Conference (for more on that check out this brilliant essay) Keynesian economics ruled the day, heralding a period of relative growth and prosperity in the United States and around the world. (The success of anti-colonial movements in Africa and Asia no doubt had something to do with these growth rates as well.) As the world switched (with the help of organizations like the International Monetary Fund) to Friedmanism in the 1980s, the effects were disastrous even in terms of economic indicators like growth rates and wages - let alone poverty indicators such as deaths by hunger and preventable disease.

But the system did work well for a few. While worries about inflation were effectively used to undermine wage growth, CEO salaries were allowed to skyrocket. Cutting taxes on capital gains and other kinds of income gave us one of the most regressive tax systems in the world, meaning you tax poor people at higher rates than you tax rich people. A government survey that came out in August showed that most corporations - including very large and profitable corporations - effectively pay no taxes at all.

What brought the system down was not public anger at the injustice of it all, it was that the system could not self regulate even in its own interest. The shock has been so bad that it's there's no chance of reestablishing that regulation - rather we must go back to an explicitly state-driven (as opposed to merely a state-regulated) form of capitalism.

Today's news confirms that Friedmanism is dead both in the U.S. and around the world, and that there's no going back. The obvious question remains: Is that a good thing for those of us who care about ending the violence of poverty and establishing a more just and democratic economic system where human need is prioritized over corporate greed?

No comments:

Post a Comment